3-2-1nsight: Falling Back to Earth

3-2-1nsight: Falling Back to Earth

How pandemic growth companies are reverting to the mean

Welcome to 3-2-1nsight from Marketing Sciences.

We have had 18 new subscribers join since the last newsletter. Welcome, and thank you for subscribing. If you like what you’re reading, please continue sharing it with your friends or colleagues, as that’s the only way to grow this newsletter.

Happy Lunar New Year! This is the first newsletter for 2022, and we have a lot to cover. Yesterday was the wrap of January, and as the old adage goes, how January goes, the rest of the year flows. Now that we’re on almost year 3 of the pandemic, I break down how we should start looking at the economy so far.

3 Stories

As the rest of the world continues to stick with their pandemic behaviors due to COVID restrictions stemming from Delta and Omicron, we’re seeing what happens to the countries that may not have had the same spike in behavior adoption that the US did during the pandemic. Instead, with its vaccination rates and social fatigue of dealing with the pandemic, the US sees a reversion to the mean.

Streaming video no longer impresses investors: What's next?

Streaming companies took it on the chin when Netflix released its quarterly results. Despite dropping a variety of hit shows, missing subscription numbers perplexed everyone, including the leadership at Netflix. Their old message of owning the relationship and creating content for their buffet-style (a very techy way of describing oneself) may have finally run tired as these results come back. Instead, Netflix may very well showcase it’s just another media company with a loyal following but does not have any greater strength than the traditional media company. Other than its description as a technology company, because its content is on an app rather than a cable bundle, Netflix has more in common with NBCUniversal than it likes to admit. As any savvy media executive will tell you, the content game is challenging, and it’s not as profitable as the scale that actual technology companies unlock.

")

Peloton internal docs show it slashed 2022 sales goals for apparel unit

Every day there’s just more news leaking about how sloppy Peloton is as a company. Rather than use the pandemic bump to help fix internal processes, the company just used that to continue its bad habits. The mismanagement of their supply and demand will one day become an HBS case study on how not to run a supply chain and how to destroy brand value as fast as humanly possible. While there are too many things to pick, seeing how Peloton misunderstands its brand and decisions, choices stick out as the most obvious in their efforts of moving into apparel. The athleisure category is still growing and massive as we saw; Lululemon is now also on track to be the most prominent women’s activewear brand despite Nike’s investment and effort into its women offerings. But Peloton threw away all of its brand value and cache when it chased growth by trying to appeal to a broader audience that didn’t care, want, or value their offering. Rather than solidify and strengthen their brand to better win at apparel, Peloton chased growth that wasn’t there.

2 Takeaways

Many pandemic growth darlings are dealing with their new reality, and the public is no longer satisfied with old-growth messages.

When the pandemic first hit, society had a lot of insecurity. For some of the tech giants that became regular parts of our life like Zoom or Teams, it made sense for those companies to see sky-high valuations overnight because of the sudden spike in demand and use of those services. That then trickled over to businesses that were not special but just seemed to have an iota of better efficiencies in a locked-down environment.

Companies like Door Dash were always terrible businesses, to begin with, that never had the unit economics of efficiencies in place to scale and reach a point of profitability. Instead, because of the lockdown, there was excessive demand, kicking the efficiency can down the road, letting these unsustainable businesses continue to run unsustainably.

Now, as these pandemic darling companies like Door Dash and Peloton find their stock below their IPO, the reality is kicking in. As the world properly opens back up, many of the adapted behavior changes from the pandemic are changing. Money saved for vacations spent on a sofa instead is going away. Many consumers watch all the hours of Netflix that they could and will not stop traveling or seeking experiences. The money associated with those behaviors will route itself back there. The growth driven by the pandemic behavior change is going away, which means any company that had a traditional sales business that just adapted to selling online is in trouble because the cost to win that consumer will only increase.

Beware of misinterpreting behavior change with behavior adoption.

Before the pandemic, Netflix dealt with the most haters. Everyone saw that its ballooning investment and costs for creating content were unsustainable. Even though society knows streaming is the future, what is the actual price of that behavior, and what’s the real value of that?

As Netflix stumbled out of the gates this year, missing first-quarter subscriptions numbers, we’re seeing the potential reality of that value. And to no fault of Netflix, who’s been working hard to make its business model sustainable change internal processes and culture to reflect the reality of its business, the market is no longer happy with those outcomes. Despite adding 54 million new subscribers during the pandemic years, winning multiple film awards, and entertaining so many families during the past two years, we can see that the stock has lost almost all that value.

Now, I’d like to bring us back to the question of valuing these new behaviors. Especially when we see companies like NBCUniversal doubling their content spend, or Disney considers selling off its ABC and ESPN entities so that they can value themselves as a technology company rather than a diversified conglomerate. When everyone discussed how connected fitness was the death blow to gyms, we’re now seeing Peloton halt production on all devices because they have too much supply and not enough demand.

Probably Won't Sell It - TheStreet")

Like all things, when it is the trend, everyone will try to rush to that latest trend and even misinterpret adaption as a permanent change. The pandemic became the world’s best global experiment of understanding and seeing firsthand the power of change vs. adoption and the aftermath of that. So far, the results don’t seem promising, as the latest research showcases that behaviors that started during the pandemic don’t last but reinforce habits already in play.

1nsight

The focus of 2022 will be on incremental growth.

When we look at the state of the world so far in 2022, we do not see too many good signs. The S&P in January closed out the month down 5.3%, which was the worst since March 2020 (the start of the pandemic). And if we look at past trends, a down January is a sign that it’ll be a rough year ahead. And as consumers potentially move back to old habits rather than continue their new adopted pandemic-driven behaviors, we can assume that many businesses that were on explosive growth trajectories will come back to earth.

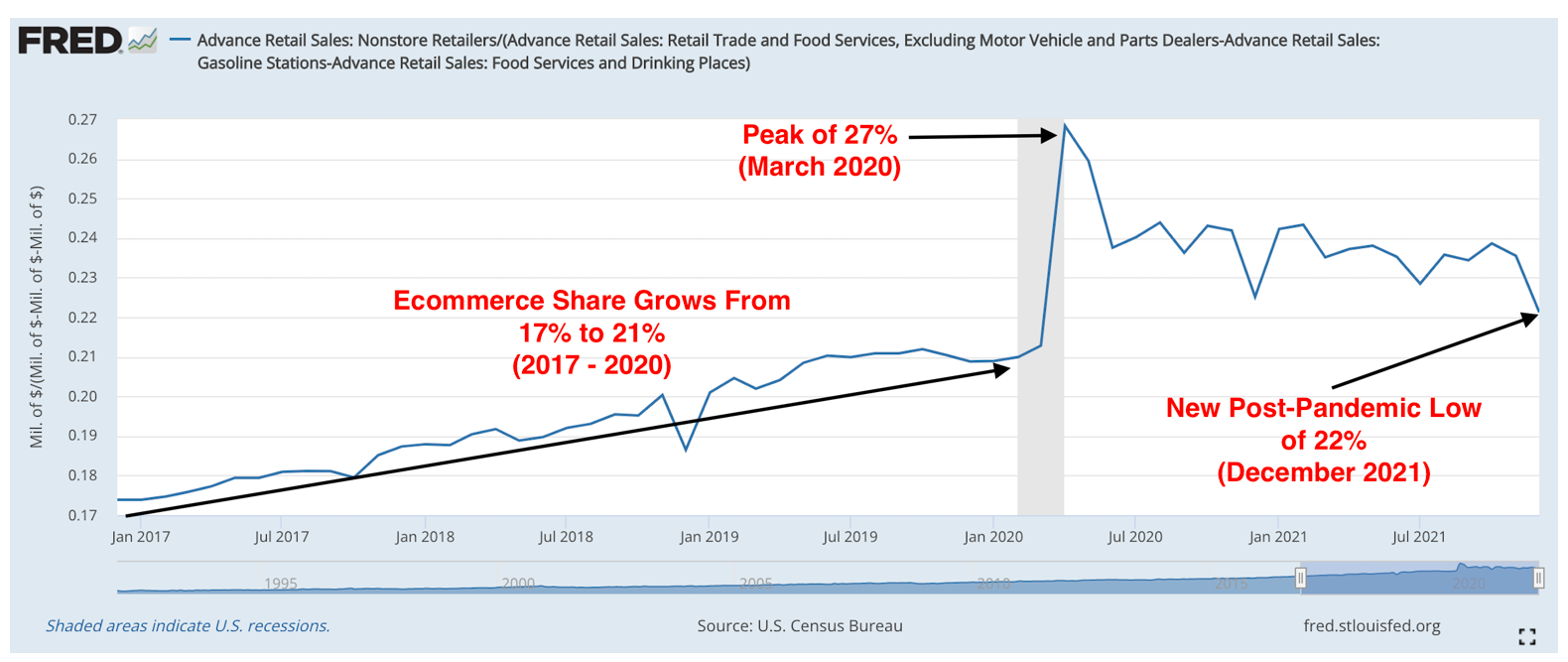

Especially when we look at results from eCommerce, we can see that despite the dramatic increase in eCommerce sales during the pandemic, that share has come back to pre-pandemic levels.

We collectively thought and believed that all the changes made during the pandemic would stick, and some have (here’s looking at remote work). Still, despite the improvements that stem from those behavior changes, the velocity and stickiness of those habits have not persisted.

Instead, the adoption rate of many behavior changes has come back to their original projections without a pandemic. Except, now that there is a model to compare results to, so many companies will find themselves under immense pressure to maintain and replicate those results, which isn’t just possible. Along with unknowns driven by global supply chains, monetary flow, and fiscal need, the cream will further separate, leaving everyone else fighting for the scraps.

So instead of trying to masquerade growth, I recommend most businesses to go back to their 2019 business strategy but accelerate it. Don’t chase growth that isn’t there. Chase the now available efficiencies instead because we all know that trends never last… but fundamentals do.